Q1 2026 Data Show Impacts of Gulf Crisis: Ahead of CSC Live 2026 in Hamburg

Disclaimer

It is important to note that the full impact in March of the Gulf Crisis is unlikely to be entirely reflected in the first quarter 2026 data. This is because many Gulf-bound containers shipped in early March, despite potential delays or diversions, would still have been reported against their intended destinations within the reporting period.

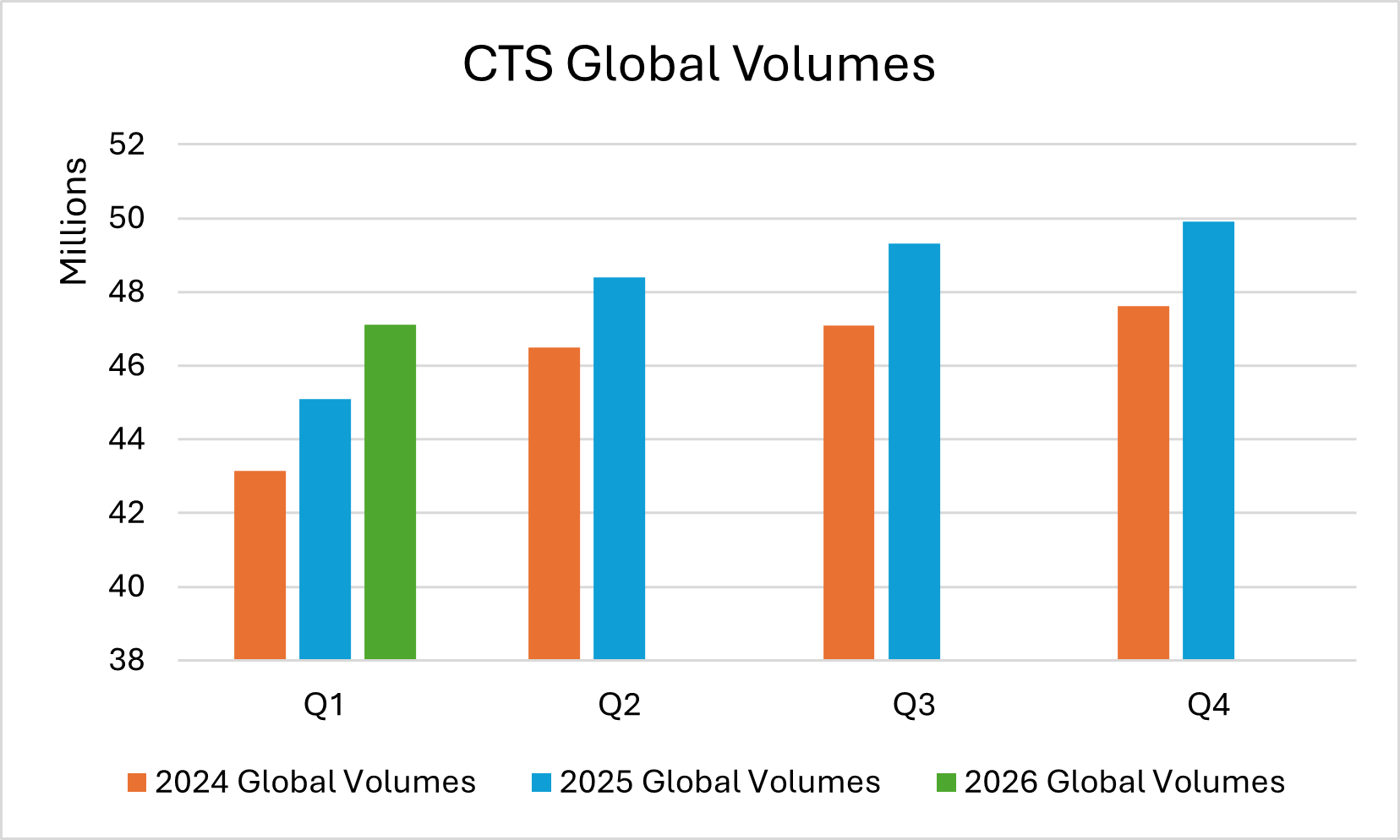

Global Volumes Remain Strong on a Quarterly Basis

With our latest March 2026 data now live, the first quarter of 2026 has come to a close, and it has proven to be one of the most unexpected starts to a year in recent memory. March 2026 figures are the first to begin reflecting the early impacts of the Gulf Crisis and the disruption surrounding the Strait of Hormuz.

For Q1 2026, global volumes reached 47.2 million TEUs, representing a 4.4% increase compared with Q1 2025. It is once again important to remember that Q1 2025 was significantly impacted by the first major alliance reshuffle in five years, with most alliances restructuring simultaneously, creating an unusual comparison base for this year’s figures.

Looking at March in isolation, global volumes increased 5.8% month on month, but declined 2.4% year on year, highlighting the early impact the Strait of Hormuz conflict is beginning to have on global trade flows.

Figure 1: CTS Global Container Volumes (2024–2026)

Regional Exports

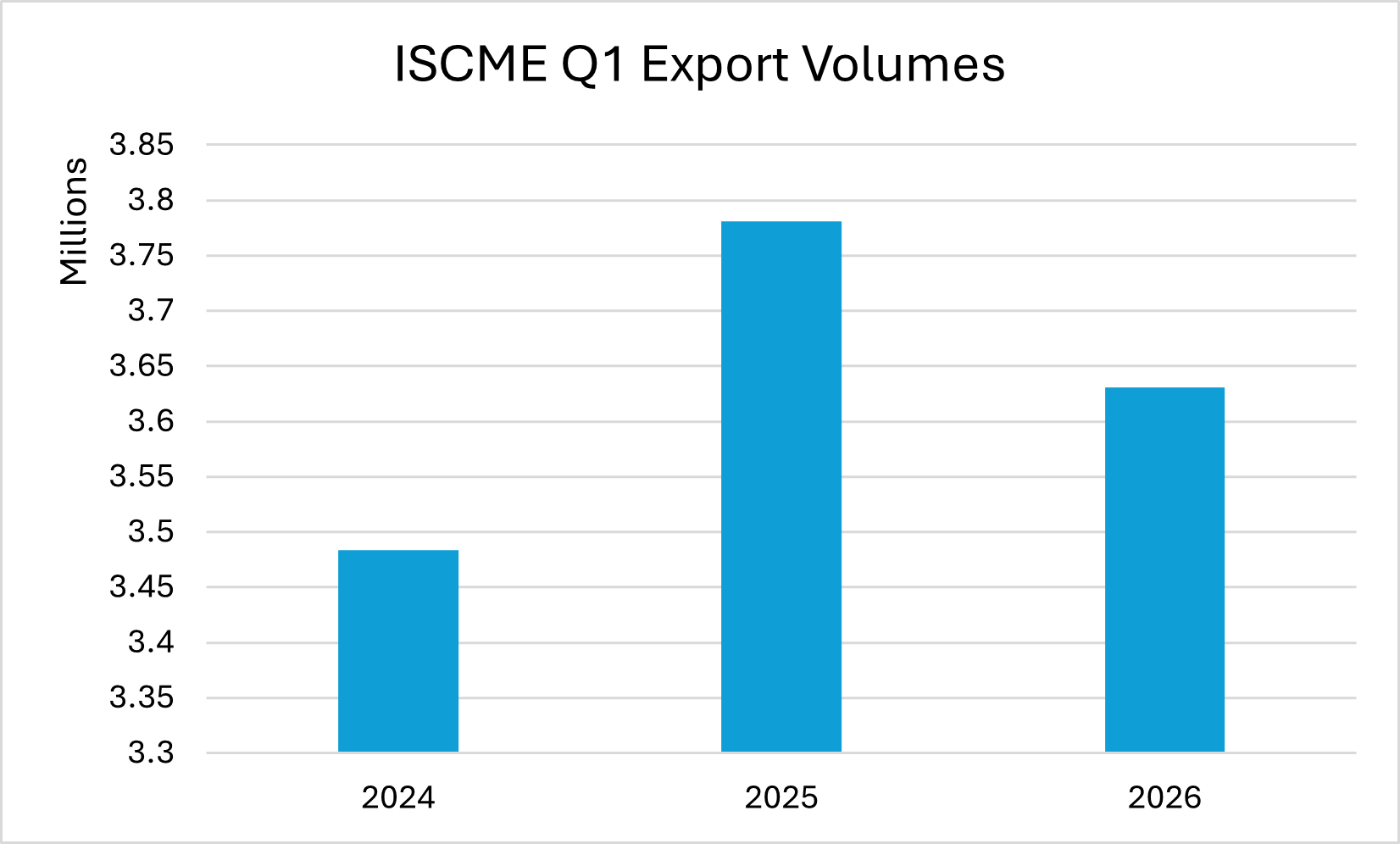

Most regional exports recorded healthy increases in Q1 2026 compared with the same period in 2025. However, Europe and the Indian Sub-Continent & Middle East were the only regions to record overall declines, down 3.2% and 4% respectively.

The decline in Indian Sub-Continent & Middle East exports is particularly significant given the region had recorded growth of over 9% in January and February compared with 2025 levels. However, the sharp deterioration seen in March as a result of the Gulf Crisis heavily impacted the quarter overall. Prior to March, nearly all import regions had been recording double-digit percentage increases for cargo originating from this region.

Looking specifically at March 2026, exports from the Indian Sub-Continent & Middle East fell by nearly 29% year on year alone, underlining the immediate disruption the crisis has had on one of the strongest-performing regions in recent years.

Figure 2: CTS ISCME Export Volumes on a Quarterly Basis (2024-2026)

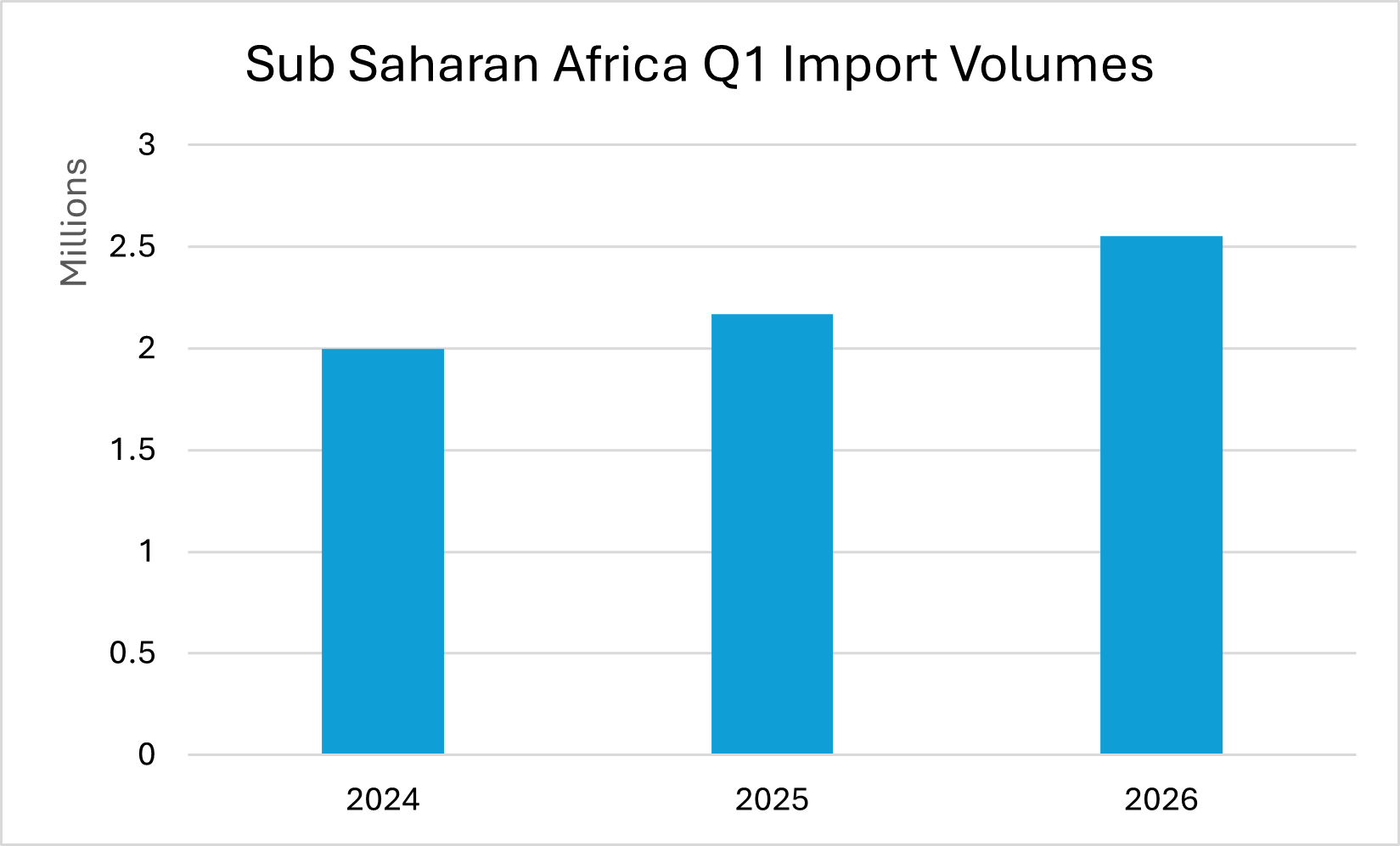

Regional Imports

On the import side, North America was the only region to record a decline in Q1 2026, down 3.8% compared with Q1 2025. In absolute TEU terms, approximately 130,000 fewer TEUs were imported from the Far East for North America during the quarter. Given the ongoing tariff implications and economic uncertainty surrounding North American trade, this pullback may not come as a major surprise.

In contrast, Sub-Saharan Africa continues to emerge as one of the strongest-performing regions globally, with imports up an impressive 17.7% in Q1 2026 compared with the same period in 2025. Nearly all exporting regions recorded increased cargo flows into Sub-Saharan Africa, with the exception of Australasia & Oceania.

The strongest contributor to this growth remains the Far East, with the Far East–Africa trade up by over 30% in Q1 2026. This further reinforces the growing importance of emerging trade lanes in supporting global volume growth amid disruption elsewhere in the market.

Figure 3: CTS Sub Saharan Africa Import Volumes on a Quarterly Basis (2024-2026)

Heading Into Further Turbulence

As Q1 2026 concludes, there is still much uncertainty surrounding the full market impact of the Gulf Crisis. Current CTS data suggests that the conflict has already removed approximately 840,000 TEUs from global volumes in March alone. As noted earlier, this reflects only around three weeks of impacted data, meaning the broader effects are likely to become more visible in the coming months.

Freight rates are expected to continue rising as carriers seek emergency routing solutions and longer transit alternatives. At the same time, increasing oil prices are likely to place additional pressure on consumer demand, which is something that has historically had a direct knock-on effect on global volumes.

There is still much to discuss and analyse as the situation develops. Our CEO, Nigel Pusey, will be speaking at CSC Live 2026 during TOC Europe 2026 on Tuesday 19th to the 21st of May, where he will explore the data behind this geo-economic disruption in greater detail. Alongside industry panellists, many discussions will focus on what the market may expect next and how stakeholders should prepare for the months ahead.

With uncertainty continuing to build, the industry will be watching closely to see how global trade patterns evolve throughout the remainder of 2026.

For a more detailed analysis of specific regional trades and to gain further insights into our findings,

please contact us on

sales@containertradesstatistics.com

For more information or to register for CSC Live 2026, visit

www.csc-live-event.com.

Stay informed and ahead of the curve with CTS – your trusted source for global container trade statistics.